French Inheritance Tax 2023:

What UK residents need to know

For UK residents who own assets in France, the French inheritance tax (or “succession tax”) can be a significant concern. The French Inheritance Tax applies to the assets of anyone who dies while domiciled in France, as well as to the assets located in France of anyone who dies while domiciled outside of France but who has French nationality.

It is important to note that not every expat who resides in France is automatically deemed domiciled in France. Specialist tax advice and domicile reports are required in order to ensure that this is the case. For many individuals, including some who have lived in France for over 20 years, UK Domicile may still apply.

As such, many UK nationals residing in France are extremely focused on French Inheritance Tax, yet fail to adequately understand or plan for their UK Inheritance Tax liabilities. This can cause serious issues for your beneficiaries when they go to complete probate in the UK. Not to mention, potentially leaving you (your beneficiaries) open to potentially large HMRC IHT bills from your estate.

French Inheritance Tax & Cameron James

At Cameron James, we specialise in providing French residents with financial planning advice, which includes UK pension transfer advice and management:

- Defined Benefit or Final Salary Pension Transfers

- Defined Contribution Transfers

- SIPP & QROPS

- Assurance VIE Advice

- General Investment Advice

We help clients maximise their existing UK pension assets. This includes achieving gross payments from SIPP or International SIPP using NT Tax codes. We actively manage old UK pension pots to maximise returns and avoid missed growth.

We do not provide French tax advice at Cameron James.

As part of our Advice Process, we will complete a detailed review of your situation (France and UK) and if required introduce you to our qualified French and UK Tax partners.

If you want to maximise your UK pensions, investments, or Assurance VIE, while ensuring correct French and UK Inheritance Tax setup, we are the right fit.

However, it is important to note, that if you have specific concerns regarding French Inheritance tax but are simply seeking a brief 20-minute telephone call to resolve complex issues, then we are unlikely the most suitable firm to address your needs.

We provide strategic financial planning advice tailored to your situation in France and/or the UK. Resolving Inheritance Tax concerns requires thorough analysis and proper planning.

Our services at Cameron James have a minimum advice fee of £3,000.

Recent Changes to French Inheritance Tax

In 2020, the French government made several changes to the inheritance tax laws that may impact UK residents with assets in France. These changes include:

Exemption from Death Duties

The spouse or civil partner left behind is not subject to inheritance tax. As a sibling of the deceased, you may also be exempt from inheritance tax if you meet these three requirements:

- You are single, a widow(er), divorced or separated at the time of the death

- You are over 50 years of age or disabled at the time of the death

- You have lived continually with the deceased for the five years preceding their death

Increase in the Tax-Free Allowance for Children

In 2020, the tax-free allowance for children rose from €100,000 to €150,000. This higher allowance reduces inheritance tax owed.

Introduction of a New Tax-Free Allowance for Grandchildren

A new €1,000 tax-free allowance for grandchildren was introduced in 2020. This applies alongside the allowance for children.

French Inheritance Tax Rates 2023

In France, inheritance tax depends on asset value and the beneficiary’s relationship to the deceased. There are four beneficiary categories, each with its own tax rate.

Spouses and civil partners

Spouses and civil partners are exempt from the French inheritance tax.

| Relationship with Deceased | Tax Rate |

|---|---|

| Spouse or child | Exempt |

| Child | 0% to 20% |

| Sibling | 35% |

| Niece or nephew | 55% |

| Other | 60% |

Direct descendants

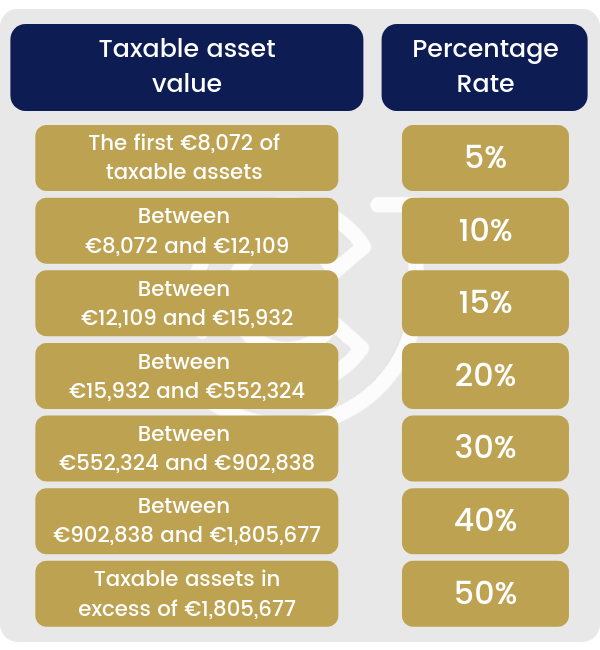

This category covers children, grandchildren, and great-grandchildren. Tax rates for direct descendants depend on the asset value inherited.

| Value of Estate | Tax Rate |

|---|---|

| Up to €8,072 | 5% |

| €8,072 and €12,109 | 10% |

| Between €12,109 and €15,932 | 15% |

| Between €15,932 and €552,324 | 20% |

| Between €552,325 and €902,838 | 30% |

| Between €902,839 and €1,805,677 | 40% |

| Above €1,805,677 | 45% |

Siblings

The tax rate for siblings is the same as for direct descendants, but the tax-free allowance is lower.

| Value of Estate | Tax Rate |

|---|---|

| Less than €24,430 | 35% |

| Over €24,430 | 45% |

Relatives up to the fourth degree inclusive

These relatives are taxed at a flat 55% rate.

Other beneficiaries

This category includes all other beneficiaries, such as friends, distant relatives, and unrelated parties. The tax rate for other beneficiaries is a flat 60%.

Impacts of French Inheritance Tax 2023 on UK Pension Members

The changes to the French inheritance tax system will have implications for UK pension members who have assets in France or who are considering purchasing property in France.

For UK residents with French assets, the increase in the tax-free allowance for non-residents from €1,594 to €100,000 is significant. This means that UK residents with French assets will have a higher tax-free allowance and pay less tax on their French assets.

For UK residents who are considering purchasing property in France, the changes to the inheritance tax system may make France a more attractive option. The increase in the tax-free allowance for non-residents, combined with the reduction in the tax rate for siblings and nieces/nephews, could make it easier for families to pass on their assets to future generations.

What is French Inheritance Tax?

More commonly known as ‘French succession tax’ or ‘droits de succession’

Inheritance Tax in France applies to those inheriting assets or gifts from French residents and is calculated progressively. This is unlike UK Inheritance Tax, which has a flat rate of 40% on all assets above £325,000 or £650,000 for married couples.

Should you be resident in France at the time of your death, or at the time you made a gift, then the inheritance will be subject to the French inheritance tax regime. Therefore, citizens of the UK or other countries retiring in France will generally have their estate taxed according to French inheritance law.

You are likely a French resident for tax if one of these applies:

- You usually spend at least 183 days of each year in France

- Your spouse and children typically reside in France, even if you spend most of your time in the UK or another country

- You work in France or receive the majority of your income from a French source

- Most of your significant assets are located in France

What is French Succession Tax?

The French equivalent of UK Inheritance Tax (IHT)

It is crucial to make clear that French Succession Tax and French Inheritance Tax are the same things; they are not two separate taxes. The official name of IHT tax in France is ‘droits de succession’ and so many English speakers refer to this as French Succession Tax. French Succession Tax differs from French Wealth Tax, which is an annual tax on assets exceeding €1.3M.

Differences between Inheritance Tax France & Inheritance Tax UK

Heterosexual Couples

Spouses and civil partners in France have the right to inherit their share of the estate free of tax, regardless of the size of the estate. Both heterosexual and same-sex partners in France can enter into a civil partnership, unlike in some other countries.

Lifetime Gifts

In France, gift tax may apply to any gifts made during a person’s lifetime. While in the UK, IHT laws only tax gifts made in the last seven years of a person’s life. This law means gift taxes are likely to be higher for you in France.

French Inheritance Law

France taxes the estate differently depending on who is inheriting each asset. French law stipulates the value of a person’s estate is the value of the assets they own in their name, plus 50% of the value of assets jointly held with their spouse or civil partner.

French Succession Rates

The French taxation regime includes different tax bands rather than taxing it all at a flat rate like in the UK. Each beneficiary receives a personal allowance. Spouses and civil partners inherit all assets left to them completely tax-free. There is, however, also a generous personal allowance of €100,000 for the children of the deceased.

Inheritance Tax Rates in France?

There is a progressive banding system for Inheritance Tax France

The inheritor first receives a tax-free allowance, and any remaining share of the estate is then taxed. The level of the allowance and the tax rate depend on the value of the assets and which relative is inheriting.

Example – Leaving €115,000 To Your Child

The Inheritance Tax Rates in France would be a total tax liability of €1,240.95, as calculated below:

- No French Succession Tax on the first €100,000

- 5% of the amount between €100,000 and €108,072, which gives €403.60

- 10% of the amount between €108,072 and €112,109, which gives €403.70

- 15% of the amount between €112,109 and €115,000, which gives €433.65

Assets Left To Other Relatives

While there is a generous €100,000 allowance for children, French succession tax is less charitable to other relatives:

- For brothers or sisters, the tax-free allowance is €15,932. The first €24,430 is taxed at 35%, the remainder at 45%.

- For nephews and nieces, the tax-free allowance is €7,967. Any amounts above this allowance are taxed at 55%.

- For non-relatives, sometimes called concubines, the allowance is €1,594. Anything above is taxed at 60%. Step-children count only if legally adopted.

Children with handicaps receive additional inheritance tax rates in France with a further allowance of €159,325. As such, people with a disability have a tax-free allowance of up to €359,325. This combines the €159,325 handicapped child allowance with €100,000 from each parent. Inheritance tax allowances in France did not increase in 2018 or 2019 and have remained unchanged since 2012. They have not received annual index-linked adjustments.

Inheritance Tax France 2018

French IHT Rates Remain Unchanged

The previous rates of Inheritance Tax France 2018 still remain in force in France. Inheritance Tax France 2019 allowances have not increased and received no index-linked adjustments, unlike many other countries. In-fact, the rates of Inheritance Tax France have remained unchanged since 2012.

Inheritance Tax France 2019

There Has Been No Uplift Since 2012

As outlined above, Inheritance Tax France 2019 rates have remained unchanged since Inheritance Tax France 2018. No indexation or increases have been applied to allowances since 2012. With unchanged allowances and rising French inflation, Inheritance Tax France 2019 is arguably more expensive than 2018. (Reuters, 2019).

UK France Double Tax Treaty Inheritance

This Treaty Mitigates Against Double Taxation

A double tax treaty currently exists between the UK and France. This UK France double tax treaty inheritance mitigates the possibility of you being subject to double taxation on a range of matters including inheritance tax (Gov.UK). The UK-France double tax treaty was most recently updated in 2008.

There is also a further tax consideration in regards to the French Wealth Tax.UK nationals entering France are exempt from wealth tax for five years on assets outside France. You can reuse this exemption if you leave France for at least three years and later return as a resident. This could significantly reduce your wealth tax liability if you have only just arrived in France.

What are the laws regarding lifetime gifts in France?

Gifts In France Are Your Lifetime – Unlike The UK 7-Year Rule

You can make tax-free gifts every 15 years, with different allowances depending on the relative. As with UK inheritance tax, one way of mitigating the tax liability is to gift some assets during your lifetime. Once again, there are various allowances for different relatives. Anyone can give up to €31,865 every 15 years tax-free, as long as the recipient is aged 18 to 80.

Inheritance Tax in France

Napoleonic Law

French law requires you to leave a significant share to your children as French succession law includes a system of ‘forced heirship’. This law has been on the statute book for 200 years. This Napoleonic law means that you need to leave at least the following proportion of your estate to your children:

- If you have one child – 50%

- If you have two children – 66%

- If you have three or more children – 75%

If one of your children dies before you, their children inherit the share their parent would have received. If that child has no children, their portion is redistributed among your surviving children. If you pass away without any children, your spouse can inherit your entire estate, even if your parents are still alive.

If you are resident in France as an Expat when you die, the tax authorities will consider that all of your worldwide assets will be subject to the forced heirship law. Except for real estate located outside of France.

Whether you live in the UK, France or anywhere else, it is essential to make a will. A will ensures your global assets are distributed according to your wishes. This also spares your family any additional aggravation dividing your estate. If you die intestate in the UK, any surviving spouse is the principal beneficiary; but in France, a spouse can inherit no more than 25% of the estate of someone who dies without making a valid will. Children and grandchildren have the first rights to inherit under French intestacy laws.

Is UK Inheritance taxed in France?

There Is A Double Tax Treaty

As outlined above, Inheritance Tax France and Inheritance Tax UK are two separate things. Where you or your beneficiaries will be subject to IHT will depend upon your residency and where a person was domiciled at the point of death. For example, if your father was UK-domiciled for IHT, his estate is taxed in the UK regardless of your residence. The UK-France double taxation treaty prevents double taxation.

Inheritance Tax France Non-residents?

Did You Make Gifts While Residing In France

If you are non-resident in France, then you may have no French succession tax to pay if you no longer hold assets in France. However, if you don’t reside in France but have assets located in France, the succession tax will likely be levied on those assets. Additionally, if you don’t live, you may still need to consider if you made any gifts while you were resident in France.

Getting the Right Help

Navigating the complexities of French inheritance tax is a significant concern for UK residents owning assets in France. At Cameron James, we are UK Pension Specialists and provide expert UK pension transfer financial advice. This includes helping expats to explore their UK Defined Benefit (DB) and Defined Contribution (DC) pension schemes to SIPP or QROPS. However, it's important to note that we do not provide tax advice.

When it comes to tax matters, we will always ensure you talk with our trusted tax partner in France or the UK. They possess the necessary expertise to navigate the intricacies of the French inheritance tax system, ensuring compliance and optimising your financial situation.

Although we do not provide tax advice, Cameron James offers full support and guidance on UK pension transfers to France. Trust us to help you make informed decisions regarding your pension while a trusted tax adviser handles the intricate details of your French inheritance tax obligations.

Book a free initial consultation today for reliable UK pension transfer financial advice with one of our IFAs, and let’s work together to achieve your financial goals.

Disclaimer: Cameron James are not tax experts and due to the complexities of the tax system and your aims and objectives it is highly advisable that you seek an independent tax opinion. You understand that Cameron James are not tax advisers and cannot be held responsible if any tax authority makes a future claim against you.