If you hold an STM Malta QROPS or STM Gibraltar QROPS, there is a design feature you need to understand before you assume you’ve done “good estate planning”.

In many STM QROPS structures, death becomes a liquidation event. Despite paperwork that appears to offer “options”, the practical outcome is often the same: beneficiaries cannot continue the arrangement in a pension-style wrapper with invested funds and flexible drawdown.

For internationally mobile families, and especially US-connected clients, that loss of control can be a serious planning flaw.

In this blog we explain:

- how STM QROPS death benefits typically operate in practice

- why this can be inferior to better-designed alternatives

- why the issue is magnified for international and US-connected families

- how Cameron James reviews STM QROPS and, where appropriate, helps clients transfer away to a more suitable structure

Key takeaways

- Many modern pensions allow beneficiaries to keep assets invested and take withdrawals over time.

- In many STM QROPS setups, death can trigger forced encashment (or a move to trustee cash with restricted withdrawals).

- “Choice” on a form is not the same as real flexibility in outcome.

- For US residents / US beneficiaries especially, losing timing control can create additional reporting and tax-characterisation complications.

- If the death benefit design doesn’t match your objectives, a structured review (and potentially a transfer assessment) is sensible.

The headline issue: no true pension-style continuation on death

A well-designed pension wrapper (a UK SIPP is the obvious benchmark) typically aims to make death not a forced exit. Instead, beneficiaries may be able to:

- keep assets inside a pension-style wrapper

- remain invested

- withdraw income flexibly over time

- manage tax and cashflow across years (rather than being forced into a single event)

- integrate the pension into wider estate planning

By contrast, many STM QROPS arrangements operate very differently. Based on the scheme death benefit documentation we commonly see, beneficiaries often do not receive a genuine “beneficiary drawdown” equivalent where the wrapper continues in a pension-like form.

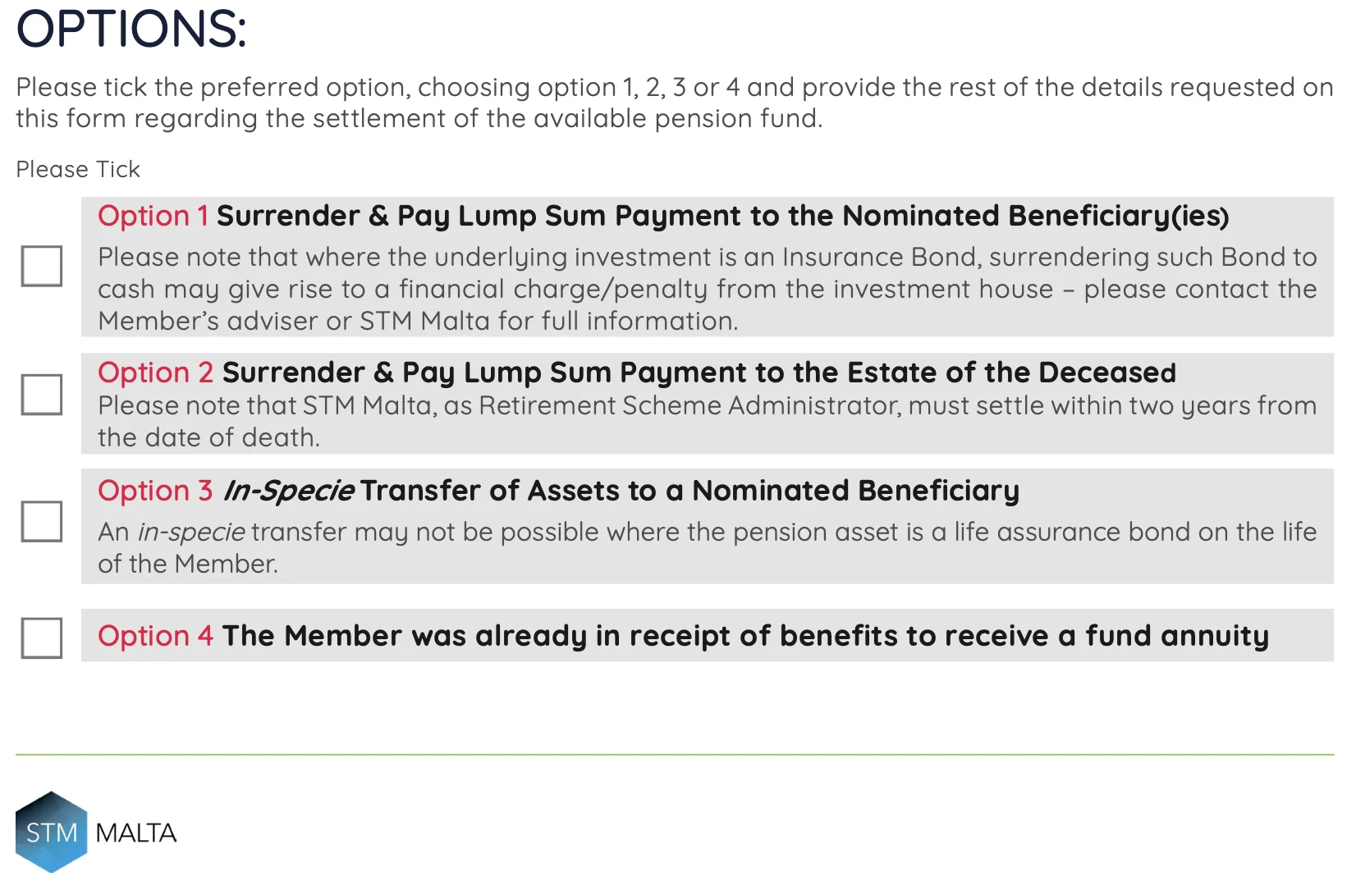

What STM offers on death (and why it can be misleading)

STM death benefit forms typically present multiple options. On the surface that looks flexible. The issue is that, once you test each route, the outcome frequently converges on encashment (or cash-based holding) rather than continuation.

Below is how the options typically work in practice.

Option 1: Surrender and pay a lump sum to nominated beneficiaries

This commonly involves:

- surrendering underlying pension assets (often including an insurance bond structure)

- paying cash out to beneficiaries

The practical limitations:

- no continuing pension wrapper

- no ability to phase withdrawals within a pension environment

- potential exposure to surrender charges / penalties

- forced selling at a time you may not choose (poor market timing is a real risk)

This is not “pension continuation”. It is a liquidation pathway.

Option 2: Surrender and pay a lump sum to the estate

This can be worse, because paying into the estate can:

- create probate delays

- increase administration and jurisdictional complexity

- expose assets to creditor risk depending on the circumstances

- raise avoidable estate / inheritance planning issues (especially across borders)

For international families with beneficiaries in multiple countries, “into the estate” is often the opposite of clean planning.

Option 3: In-specie transfer to beneficiaries

This is the most misunderstood option.

In many STM QROPS setups, assets are held via life assurance bonds. Where the bond is written on the life of the member, the scheme’s own wording may indicate that an in-specie transfer may not be possible on death.

STM’s own wording is:

“An in-specie transfer may not be possible where the pension asset is a life assurance bond on the life of the Member.”

Even when investments can transfer in specie, the key point is this:

- the assets typically transfer out of the pension environment

- they become the beneficiary’s personal holdings

- the pension wrapper does not continue in a beneficiary drawdown structure

So, even in the “best” interpretation, it may still function as asset distribution, not pension continuation.

Option 4: Annuity (only if already in receipt of benefits)

Where this option exists, it is often misunderstood as well.

Common constraints include:

- assets being sold and held in the trustee cash account

- withdrawals being limited by restrictive rules (rather than flexible drawdown)

- significant inflation risk over time

- limited ability for beneficiaries to align withdrawals with their own tax position or cashflow needs

- in some cases, the only “planning tool” is delaying withdrawals to soften a single-year tax hit

For many families, it’s not desirable, it’s simply the least-bad option available under the structure.

The practical reality: death can become a forced exit event

When you strip away the tick boxes, the recurring planning problem is straightforward:

- no meaningful beneficiary drawdown equivalent

- no long-term continuation inside a pension-style wrapper

- limited intergenerational planning control

- reduced ability to manage timing, tax, and investment strategy after death

That is a design choice, and it’s often revealed at the exact moment you want planning to work smoothly.

Why this can matter even more for US residents and US-connected families

US-connected scenarios tend to punish lack of control.

Forced encashment can create additional complications such as:

- large lump sums landing outside a recognised retirement wrapper from a US perspective

- immediate reporting and classification questions for beneficiaries

- loss of timing control over income and tax planning

- higher risk of administrative errors (and unnecessary professional costs) due to complexity

Even where tax can ultimately be managed with the right support, flexibility is the asset. Forced outcomes remove flexibility.

Are there better QROPS providers? Yes.

Not all QROPS are built this way.

Some providers are structured to support:

- genuine beneficiary continuation (pension-style wrapper outcomes)

- assets remaining invested after death

- phased beneficiary withdrawals over time

- better suitability for international families (including some US-connected planning scenarios, where appropriate)

The differences are not cosmetic. They show up when it matters: death, succession, and multi-jurisdiction outcomes.

Should you consider an STM QROPS transfer?

A transfer review may be appropriate where:

- the death benefit design is misaligned with your objectives

- beneficiaries are internationally mobile

- there is US residence/citizenship/green card status in the family

- you want long-term control rather than forced liquidation mechanics

- your arrangement no longer meets “modern” planning standards

Transfers are not automatic and must be assessed carefully, but doing nothing is still a decision, and often a costly one.

How Cameron James helps

We help UK and international clients review whether their pension wrapper is fit for purpose, and if not, what a sensible alternative looks like.

A typical QROPS-focused review includes:

1) Scheme rules review (what it actually does)

We analyse the scheme documentation and death benefit provisions based on what is written, not what anyone assumes.

2) Cross-border beneficiary planning lens

We map likely outcomes across jurisdictions relevant to the member and the beneficiaries (including where the family is internationally split).

3) Transfer feasibility and risk assessment

If a move is potentially sensible, we assess the practical realities: trustee processes, timelines, investment mechanics, and administration risk.

4) US-connected considerations (if applicable)

Where there is a US angle, we take additional care to ensure the structure is coordinated realistically and not based on generic “expat” assumptions.

5) Implementation support (if appropriate)

If a transfer is recommended, we manage the project properly: documentation, provider engagement, and clear step-by-step handling.

The goal is not “transfer for the sake of it”. The goal is a retirement structure that protects your family’s options, not one that forces a payout at the worst possible time.

Practical next steps if you’re in an STM QROPS

If you’re reading this thinking “that’s not what I intended”, take these steps:

- Request the death benefit wording in writing and keep it on file

- Confirm beneficiary options based on the actual scheme rules, not assumptions

- Review the impact based on your beneficiaries’ tax residencies and citizenships

- Compare against alternatives with genuine beneficiary continuation (where suitable)

- Get regulated advice before changing anything, particularly with any US connection

FAQs

Can STM change these death benefit features?

Scheme rules can change, but you should plan based on the rules as they stand today, not on the hope of future improvements. If the design doesn’t fit your objectives, review alternatives.

Is a forced lump sum always bad?

Not always. Some families want a clean lump sum. The problem is when it becomes the only meaningful outcome, regardless of beneficiary circumstances.

If I’m US resident, does that automatically mean I should leave STM?

No. But it does mean you should be more deliberate about structure, classification, reporting, and beneficiary outcomes. Forced encashment can be particularly unhelpful in US-connected scenarios.

What are my options if I want better death benefits?

Depending on circumstances, options may include transferring to a different QROPS with more flexible death benefit design, or in some cases moving to an alternative arrangement where appropriate. Any change must be assessed carefully and implemented correctly.

Book a call with Cameron James

If you hold an STM QROPS and you want your family to have real flexibility, not a forced payout, we’ll review the death benefit rules with you and explain what better-designed alternatives look like (including where there’s a US connection)👇

Book a complementary call to start the review

Important disclaimer

Cameron James is not authorised to provide tax advice. For formal tax planning, we will refer you to a qualified third-party tax adviser. This article is for information purposes only and does not constitute financial, legal, or tax advice. Any pension transfer decision should be taken only after regulated advice and a review of your full circumstances.