A pension annuity is a popular alternative to workplace or personal pension schemes. It provides a guaranteed retirement income.You can use part or all of your pension pot to purchase an annuity. This secures you a fixed monthly income for life.

If you're planning for retirement, it's important to understand if a pension annuity fits your financial goals.

Before we go further, watch our short video on pension annuities. It features Dominic James Murray, CEO of Cameron James.

Watch Other UK Pension Transfer Videos in Our YouTube Channel!

What Is a Pension Annuity?

An annuity pension is a type of insurance plan. You make a one-time payment to a provider who agrees to pay you a monthly income for the rest of your life. This income is guaranteed and does not rely on a finite pool of funds, so if you live a long time, you may receive more than you paid.

The main benefit of an annuity is its consistency: you will always have an income. The main disadvantage is that this income may be less than you could earn through another method.

How Does a Pension Annuity Work?

When you reach retirement age, you can use your pension pot to purchase an annuity. It will provide you with a guaranteed fixed income for the rest of your life or a set period.

For example, you could take 25% of your pension pot as a tax-free lump sum and then use the remaining 75% to purchase an annuity. Insurance companies typically sell annuities, and your annuity income is taxed. The amount of income tax you will pay is determined by your tax bracket.

Are Pension Annuities Worth It?

You may be wondering whether annuities are a good investment. This is a question we occasionally get from clients who are thinking about retiring. They are unsure whether they should buy an annuity or have a Flexi-access drawdown of their capital over time.

We'll give you the short answer: clients are better off not purchasing an annuity and instead focusing on their investment portfolio.

An annuity, ironically, is not a type of investment. By definition, it is an insurance product. When you buy an annuity, you effectively exchange your pension fund for an annuity provider.

In exchange, they will pay you a set amount each year. Some clients will appreciate this because it provides a high level of security. They know what will happen, and there will be no surprises during their retirement. However, you must ask yourself why any annuity company would do this.

Do you think they'll risk losing money if you give them £500,000, and they promise to provide you with an income for the rest of your life? No, they will not. You will always have to pay a premium for an annuity because the company must make a profit in some way.

On the other hand, if you took the £500,000 and invested it in the stock market, your portfolio will more likely grow because you have invested it for a long time.

You'll regret it if you choose to buy an annuity over managing your investment through an IFA. Instead, you'd thank yourself for all the portfolio growth you would have over your retirement.

In general, we don't think this is a particularly smart idea, especially given that annuities aren't particularly popular these days. It's a shrinking market. It means that anyone going to the unity market to get a quote will not get a very good one. There is no longer the benefit of good quotes based on economies of scale in what is now a limited market.

Because annuity providers are not making as much money as they once did, any new clients must come in through the door or contact them online. This is due to fewer people purchasing annuities these days, which is why their fees will almost certainly be higher.

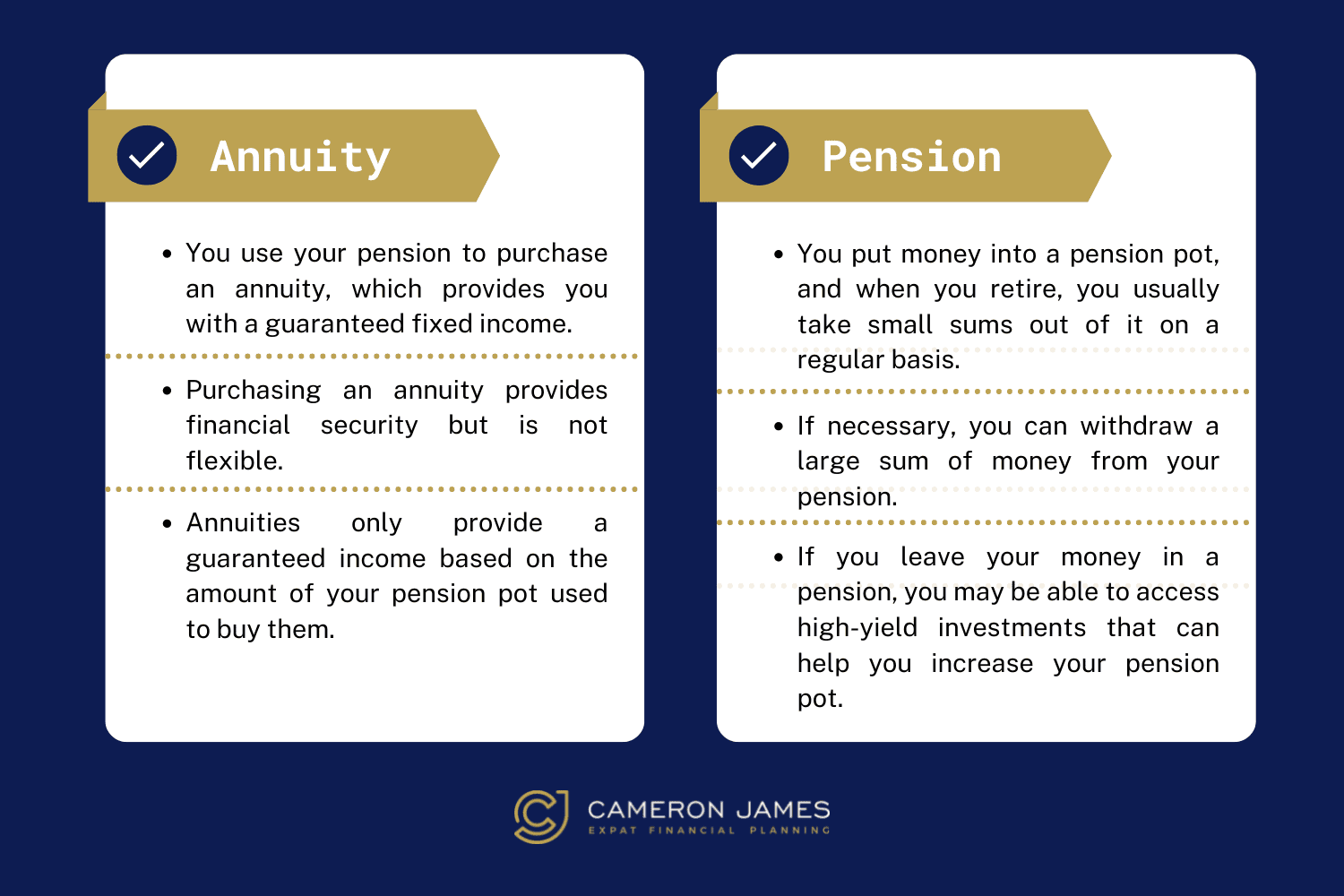

What’s the Difference Between an Annuity and a Pension?

The table below summarises the main differences between an annuity and a pension:

Our Advice on Annuity

As previously stated, our advice to most clients is to avoid purchasing an annuity. Look at the long-term return of the equity markets (FTSE 100, S&P 500) throughout 20, 30, 40, or 50 years. You will have a better return by investing your money in the stock market and taking gradual income from your pension pot.

Clients understand that investment returns will fluctuate year after year. Still, they want the same income level during retirement, just because the market fluctuates doesn't mean you can't have the same income level in retirement.

If you have £500,000 but want £20,000 per year in retirement, you can still take £20,000 per year. The market returns will differ within your portfolio, but they should not affect your retirement.

Remember that investments are long-term investments: 5, 10, 15, and 20 years. Just because your portfolio performed well in the first five years does not mean you should increase your retirement income. You should keep it at £20,000.

Similarly, just because the markets haven't performed well in the first five years, that doesn't mean you should withdraw less money from your retirement account. You should still withdraw the annual £20,000.

More importantly, with flexible investments, you can tell your IFA that you don't need the £20,000 this year if you still have money left over from last year. The following year, you may decide that you need more money if you have something to pay for or something to do.

Is an Annuity Right for Me?

An annuity offers benefits such as predictability, security, and ease of planning. However, it may limit your income potential and flexibility compared to other retirement income strategies. It’s important to weigh these factors carefully and consider whether an annuity aligns with your personal retirement goals.

If you're unsure whether an annuity or a flexible investment approach is right for you, our experienced Independent Financial Advisers can help. Book your free consultation today to explore your UK pension options and create a retirement plan tailored to your needs.

Take control of your retirement income now, book your free consultation with Cameron James.