If you are a member of a Final Salary pension scheme in the UK, you might have the option to retire early. This typically takes place between the ages of 55 and 60, before the normal retirement age of 65. However, it’s important to carefully consider the advantages and disadvantages, as early retirement can have a significant impact on your long-term financial security.

We will explore the concept of Final Salary early retirement and why people may take this option. We will also explain how early retirement could affect your retirement income. Furthermore, we explain why it is important to seek guidance from an Independent Financial Advisor (IFA) before making a decision.

You can watch our detailed YouTube video on this topic below. If you want straightforward explanations on pensions and retirement planning, visit our YouTube channel.

What is a Final Salary Pension Scheme?

A Final Salary or Defined Benefit (DB) pension scheme is a type of retirement plan that provides a guaranteed income for life. This is based on your Final Salary and the number of years you have been a member of the scheme. An employer usually sponsors the pension scheme, and the income paid is based on a formula that considers your years of service and Final Salary.

The formula used to calculate the pension income is usually generous, with most schemes offering a retirement income of around 1/60th to 1/80th of your Final Salary for each year of service. For example, if you have worked for 30 years and your Final Salary is £50,000, you could expect to receive an annual pension of between £18,750 to £25,000.

Early Retirement Before Normal Retirement Age (NRA)

If you decide to take early retirement before the NRA, you will usually have to pay a penalty. The penalty is imposed because you are leaving the scheme earlier than planned. The pension scheme administrators will have to make adjustments to their investment strategy to cover your early retirement benefits.

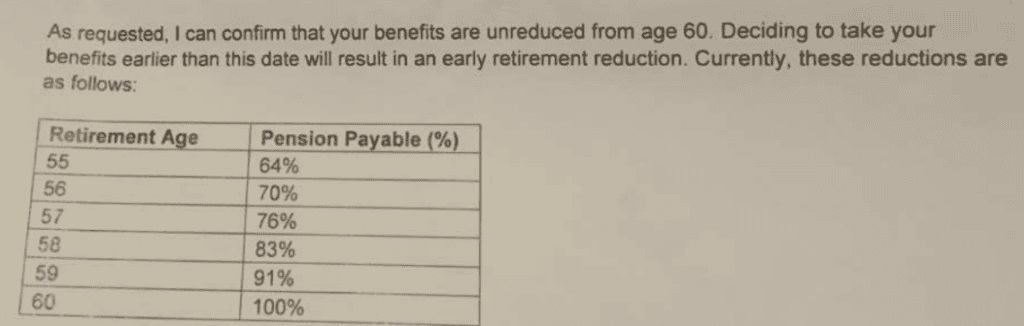

The reduction in pension income can be significant, with some pension schemes reducing your annual pension by as much as 36% if you retire five years early. This is illustrated below from a recent client of ours.

This is because when you first join the scheme, the administrators assume that the pension pot will be invested for a set period of time (until you reach your NRA). By taking your benefits earlier, the investment period is reduced, thus impacting the fund's performance.

One of the main reasons for ceding schemes imposing a penalty on early retirement from a DB pension scheme is to help reduce the scheme's liabilities. When an individual requests early retirement, they may be more susceptible to accepting an early retirement option, even if the deal offered is not particularly favourable. However, it is crucial to have a qualified IFA perform a comprehensive assessment of the scheme's particulars because the penalty can be caused by several potential factors that require consideration.

Final Salary Early Retirement at Cameron James

It's essential to consider the long-term financial implications of taking early retirement from a DB pension scheme. A rule of thumb at Cameron James is to avoid taking early retirement from a DB pension scheme. It is unlikely to be in your best interest. Pension scheme administrators typically reduce your annual pension significantly if you retire early, negatively impacting your financial security in retirement.

The key consideration for taking your Final Salary early is whether you can afford to retire early and maintain your standard of living. You need to factor in the reduction in your pension income, any other sources of income, and your expenses, such as mortgage payments, bills, and living expenses.

It's essential to plan for your retirement and create a realistic budget that considers your income and expenses. You should also consider your long-term financial goals. These include paying off your mortgage, funding your children's education, and leaving an inheritance for your heirs. This is where an IFA comes in to help you calculate and plan your retirement for your best interest.

Ill-Health or Serious Ill-Health

If you have ill-health or serious ill-health, you may consider accessing your pension pot early to support your financial needs. You have to underline that ill-health and serious ill-health are two different terms, and your ceding scheme’s rules may treat them differently.

For serious ill-health, you may be able to access your pension pot without paying the penalty. For instance, if you have less than 12 months to live or are terminally ill, the pension scheme administrators may offer you a reduced commutation factor to pay out your full CETV instead of an early retirement. A CETV is the amount you could receive if you transferred your pension to a SIPP or QROPS.

It’s important to note that the rules for accessing your pension early due to serious illness are quite technical. You should seek the help of an IFA to help you understand the rules of your pension scheme.

How Your IFA Can Help You

Deciding to take early retirement from a Final Salary pension scheme is a major financial decision. The potential penalties and income reductions mean it’s vital to fully understand your options before committing. At Cameron James, our IFAs provide free initial consultations to help you evaluate your pension scheme and plan for retirement.

Don’t risk your financial future, contact us today to get personalised advice tailored to your unique situation. Your retirement journey deserves careful planning, and we’re here to guide you every step of the way.