The quarterly review of global capital market performance and events for the first quarter of 2022. This review contains the current global event overview, a review of stock and bond asset classes in the US, UK, and international markets, a look at UK pension transfer industry, and company updates from Cameron James. All of them are presented by our CEO and Independent Financial Advisor, Dominic James Murray.

Who Saw Putin Coming?

While possibly predictable with continued growth of NATO on Putin's doorstep (despite many Western promises not to) the Russian invasion of Ukraine has resulted in the greatest humanitarian crisis since the Second World war. With many lives lost and the displacing of millions from their homes. The impact of this war has been felt globally, posing a significant challenge to the post-Covid19 pandemic recovery.

Russia’s invasion of Ukraine has drawn widespread condemnation and elicited a range of unprecedented sanctions from the US and its allies. The US was the first major country to put a ban on Russian Oil, Gas and Coal as President Biden said, “targeting the main artery of Russia’s economy.”

The Fall Of Londongrad?

Even the UK, famous for allowing Russian wealth to flow into the streets of Mayfair & Belgravia, has tightened its policy. The loopholes in UK law which have long enabled London firms to launder oligarchs’ wealth are quickly disappearing. Will this be the end of Londongrad or the ‘Moscow-on-the-Thames’ as we know it? I suspect not.

But for now, it is currently very unfashionable to be doing business or being seen to be doing business with Russia. Unless you are China or India, of course, who seem content to lock-in low oil prices no matter the bad publicity. Whether the big profit-driven corporations pulling out of Russian is for moral or PR reasons on Twitter is yet to be seen.

Russia and China, have always been a huge risk and these really events in Russia (on top of Mr Alibaba, Jack Ma, going missing in China following his remarks), have highlighted more than ever the risk that ‘emerging’ market dictators can pose on a client's portfolio. The US might have ‘high' valuations, but it's economy is controlled by more than one person.

Russian Bloodbath

Sources close to Moscow, say that Vladimir Putin is somewhat isolated and does not use any forms of social media himself. Even his family, and children, are shrouded in secrecy.

However, he will know what his economy looks like following this invasion, and it paints a sorry picture for a country that has made so much economic progress over the past decade.

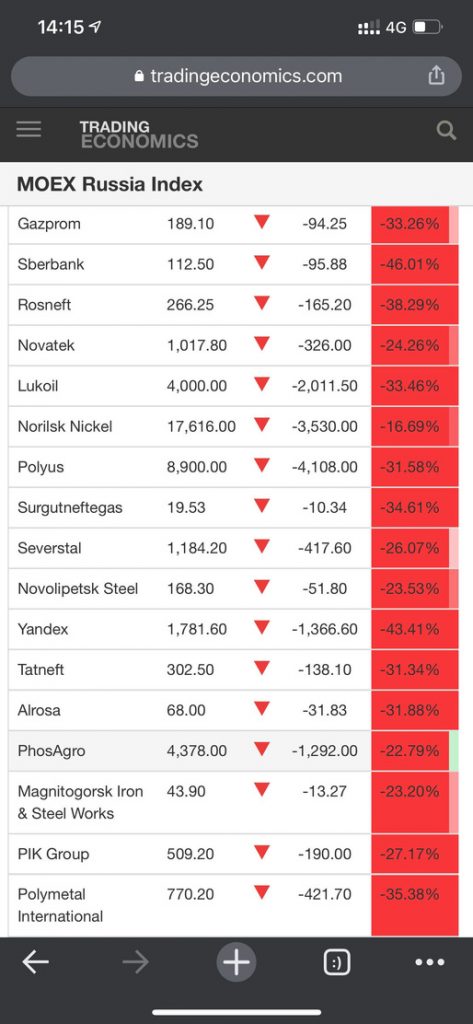

As Baron Rothschild once famously said, “Buy when there's blood in the streets…”. However, even as an Adventurous investor with a long-term outlook and a firm understanding of risk, I could not bring myself to buy the dip in the bloodbath that entailed in Russia.

Below is a screenshot I took from my phone around late February. Across my career, I have not seen such daily drops in one specific country, irrelevant of their sector or company performance.

The Oligarchs & Navalny

Putin is playing a high-stakes game, and for how long the countries Oligarchs will put up with his recent polices is yet to be seen. With every super yacht which is sanctioned or detained, the internal pressure of the Kremlin grows. Has Putin bitten off more than he can chew this time, or will he eventually prevail through the bullying and coercive tactics that saw him rise to power in the first place?

While the Kremlin controlled media has been sprouting accusations that Bucha is fake news and distracting Russians from what is really happening, Russian Authorities (aka Putin) sentenced prominent opposition figure Alexei Navalny to nine years in a “strict regime penal colony” in a fraud case which Navalny obviously rejects as entirely fabricated.

I was in Moscow and Sochi in November 2021 and saw a modern and technologically driven Russia. This latest chapter has set its economy back 10-years and there is still more fallout to come.

The EU Response

On the 3rd of April Lithuania, Latvia and Estonia (those closest) announced a ban on Russia Gas imports, the first European countries to announce such a move, putting pressure on the rest of Europe to follow by example. The EU has upcoming discussions to draw up plans on how to minimize Russian energy imports, with EU President Macron calling for bans. We expect some pushback from Germany, which are heavily dependent on Russian energy (Politico).

Sanctions also targeted the Russian financial system. Assets of the Russian central bank were frozen, while coordinated steps were taken with numerous allies to seek to deny Russia access to the global financial system. Some of Russia’s wealthiest people have also been hit with asset freezes and seizures, while a slew of major international corporations has withdrawn from the country. Numerous other sanctions have been instated (Schroders).

Global Economic Outlook

Fitch Ratings have cut its world GDP growth estimations for 2022 by 0.7% to 3.5%. They indicate the main reasoning for its reduction is higher energy prices and the tightening of US monetary policy (Fitchratings). The OECD believes GDP growth could be 1% lower and inflation 2% higher as a consequence of the Ukraine conflict (OECD).

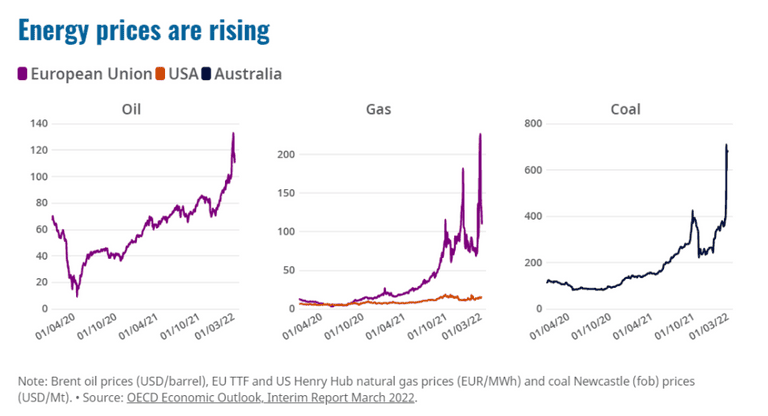

As I mentioned last quarter, inflation is rife and far above the target inflation of 2% due to supply chain distributions caused by Covid-19, but now we expect even great disruptions as a result of the Russia – Ukraine conflict. Put simply, Russia supplies around 19% of the world’s natural gas and 11% of oil. Europe is particularly dependent on Russian gas and oil, it gets approximately 40% of its supply from Russia. As you can see by the graphs below, the price of oil has nearly doubled over the last year, whilst the price of gas has increased 10-fold.

We can expect extreme price pressures to follow through 2022 before decelerating and falling below-target inflation in 2024 (Bovina, S&P Global).

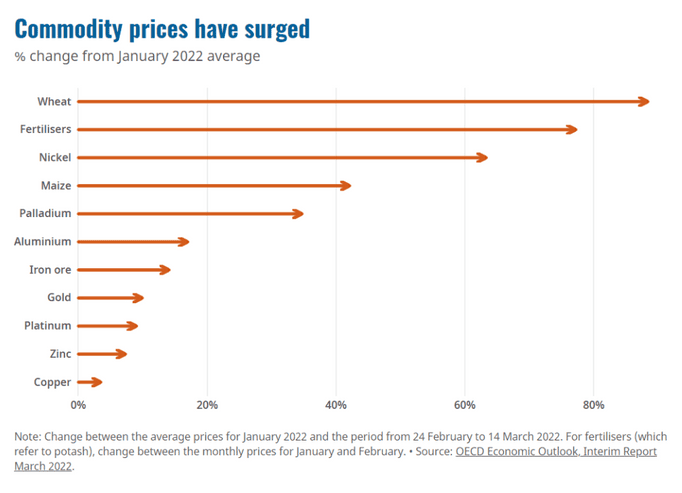

Other Commodities have also surged, Ukraine and Russia are both important producers of wheat, fertilizers, and metals. Rising metal prices could have a wider supply chain effect on industrial manufacturers such as aircraft, car, and chip manufacturing.

So, Why Is Everything Getting More Expensive?

We can see from IMF analysis that a significant driver of inflation has been rising shipping costs (IMF Blogs). The cost of shipping one container has increased a whooping 7x in the 18 months following March 2020 (IMF Blogs). This has resulted from the supply distributions resulting from Covid-19 with ship workers sick and unable to work, an inability to cross borders due to restrictions, and exacerbated demand from back-ended orders. They anticipate the inflationary impact of shipping costs will continue to pass through to domestic countries and that this impact predates the Ukraine conflict, which will only exacerbate global inflation.

Other drivers of global inflation are the increasing price of food and fossil fuels. Crude Oil is an input good that has multiple uses including transportation, heating and electricity generation, varied petroleum products, and plastics. As well as impacting consumers indirectly, the cost of oil accounts for roughly half of the retail fuel prices in the US (Federal Reserve Bank of Dallas).

Some argue that renewable energy is the solution to our inflationary problems. As commentators point out, oil and gas prices are subject to geopolitics and natural diminishment, subjecting the commodity to volatility. So, why not use solar, wind, and nuclear energy to avoid such issues in the future, this is a debate going on now in many governments across the globe, particularly in Europe who have a dependency on Russian oil and gas. For example, Germany which buys approximately half of its natural gas from Russia now plans to move up its 100% renewable target of 2040 to 2035 (Fast Company).

However, this does not offer a short-term solution to the problem. The short-term strategy could be to turn to alternative suppliers, such as Saudi Arabia, Azerbaijan and the US. The US has agreed to boost its shipments of liquified natural gas to Europe by 70%, aiming to supply 50 billion cubic metres per year until at least 2030. But that would still only be a third of what Europe imports from Russia, meaning other sources will be needed too.

In response to higher inflation, Central banks around the globe are now hiking interest rates to mitigate the situation, and we expect to see a continuation of hikes into the near future. Brace yourself for increased costs throughout 2022. The price of a G&T in London, at this year's Christmas Party, will almost certainly be a record breaker!

US Inflation

The U.S. Inflation rate accelerated to a 40-year high of 7.9% in February, matching market expectations. Energy was the greatest contributor (25.6% vs 27% in January), with petrol prices surging 38% (40% in January). Food prices had it is the largest increase since July 1981, by 7.9%. Excluding energy and food categories, the CPI rose 6.4%. Inflation was expected to peak in March but amidst the Ukraine-Russia conflict, it is likely that inflation levels will remain elevated for a longer (Trading Economics).

UK Inflation

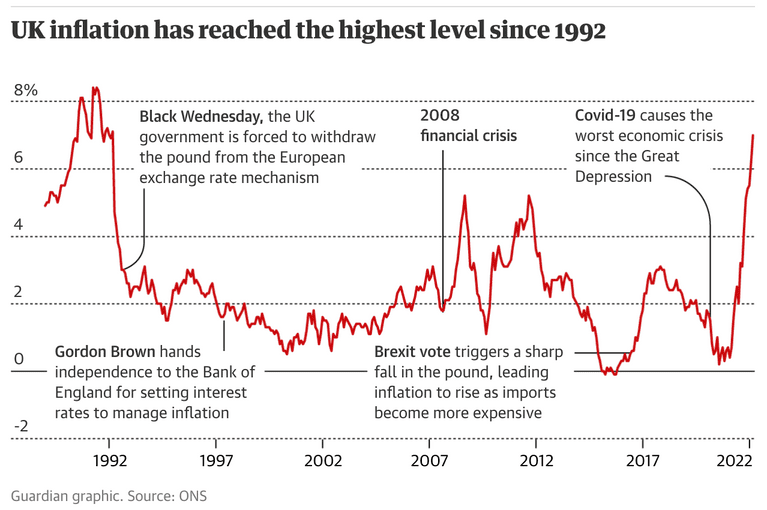

The Consumer Price Index rose by 5.5% in the 12 months up to February, an increase from 4.9% of the last twelve months in January. The greatest contributions to February’s inflation rate came from housing and household services (1.39%, predominately from electric, gas and other fuels and owner-occupier’s housing costs) and transport 1.26% (ONS).

According to the Office for Budget Responsibility (OBR), UK consumer price inflation is set to peak at close to 9% this year. The OBR published its new forecast for the Consumer Prices Index (CPI) alongside the Spring Statement at the end of the quarter. It now expects CPI to hit 8.7% in Q4 2022. Chancellor Rishi Sunak announced additional measures alongside the Spring Statement designed to support the UK consumer (Schroders).

Interest Rate Hikes – US Fed

As expected at the end of 2021, the Federal Reserve official voted for its first interest hike in three years of a quarter-point from 0.25% to 0.50% during its March 2022 meeting. Along with the hike, the Federal Open Market Committee pencilled in another increase at each six of its remaining meeting this year with a consensus pointing to 1.9% by the end of the year (CNBC), the committee sees three more hikes in 2023 and then none in the following year.

There are now some discussions between different policymakers of a 0.50% hike in the next committee meeting rather than 0.25% because of sudden inflationary pressures, but some warn this could be putting the brakes on the economy and suggest easing into rate increases.

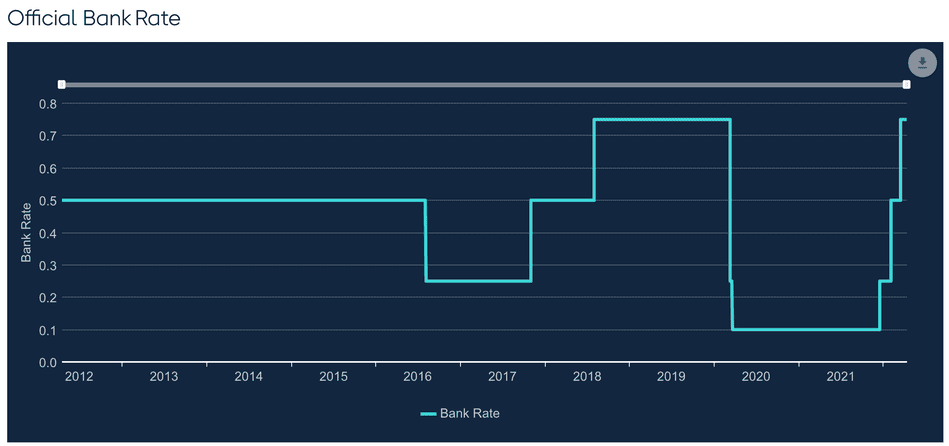

Interest Rate Hikes – UK BoE

Over the last quarter, rates have risen twice in effort to reduce inflationary pressures, moving to 0.50% on 03 Feb 22 and to 0.75% on the 17th March 2022. The BoE notes the change in interest rate will take time to take effect and that they expect inflation to reach around 8% this spring. However, would expect to reach the 2% over the next couple of years. The committee said that they may look to increase rates in the future months, depending on what the rate of inflation looks like and how the economy plays out (Bank of England). Commentators suggest UK interest rates could reach up to 1% by the end of the year.

For anyone familiar with CETVs, this means bad news for CETV values. Which will almost certainly be pushed further down over the coming years in the government attempt to reach 2% inflation targets.

For those of you have already completed your Defined Benefit Pension transfer, there is no concern. For those of you still considering, get your skates on and try to attain your CETV before the 5th May 2021, when we will likely see BoE interest rates rise again.

US & UK GDP Growth

The US economy continues its recovery and has performed well over the last few months. The unemployment rate is back to full employment, and labour participation rates have increased, with those who left the workforce during the pandemic starting to return to work (Deloitte).

UK economic recovery is underway and is nearly at pre-Covid levels, GDP is now 0.1% below where it was pre-COVID-19 in Q4 2019. UK GDP is estimated to have increased by 1.3% in Q4 2021, which is an improvement upon estimates of 1% in 2021 Q1. Overall GDP is estimated to have grown by 7.4% in 2021 (previously estimated to be 7.5%) (ONS).

The Markets

US S&P 500

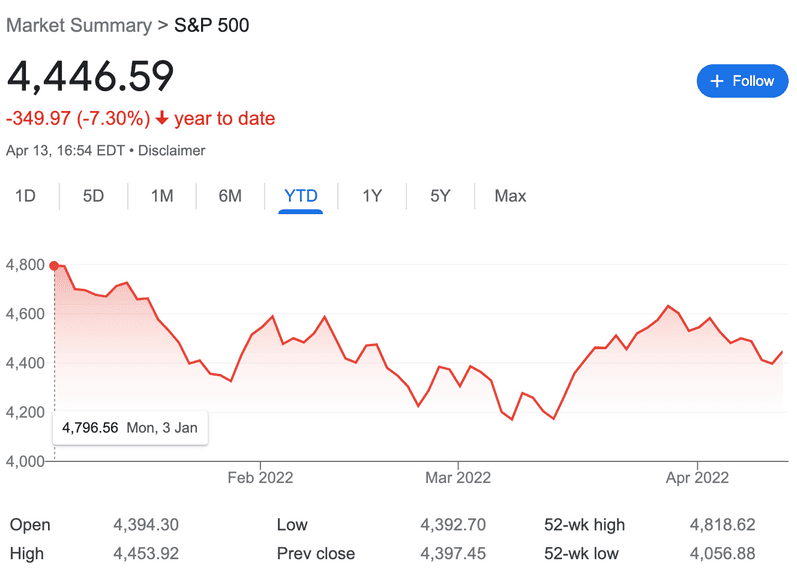

We saw about a 10% downwards correction in mid of February, most of the correction was following the Fed’s tighter monetary policy (Barrons). The FED has risen rates and is expected to do so several times later in the year to tackle inflation, this causes concerns for investors for future economic growth and businesses performance. The S&P 500 bounced back at the end of March and now is trading at a similar level to before this correction. This type of volatility is unusual, since 1945 on average it takes fourth months for a pullback of 10% to 20% in the S&P 500 (CNBC).

The volatility in the market is a result of uncertainty over what the impacts of the Ukraine-Russia conflict could bring with what sanctions could look like, pricing in what the price of oil will be, the effect on consumer spending and the resulting impact of higher interest rates.

The initial impact of rising rates have had the greatest negative impact on Growth stocks, while the impact on value stocks has been much smaller (NASDAQ). In Q1, the large-cap Russel 1000 value index outperformed the Russell 1000 growth index by more than 8%, while on the smaller-cap Russell 2000 Value outperformed its counterpoint by over 10%. For the large-cap indices, it is the greatest outperformance since the 2000-2002 era. It begs whether this is a turning point in Growth vs Value investing.

Energy, Metals, and Agriculture

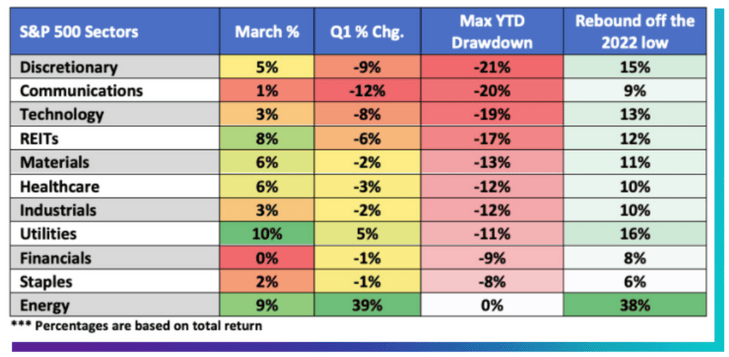

Energy, Metals, and Agriculture Commodities Continue to Surge at a Historic Rate. S&P500 Energy sector saw a 39% increase in performance in Q1, which represents the best quarter since the inception of the index in 1989 after a period of high oil and gas prices. Utilities, saw a 5% Q1 change, as markets expect electric, gas companies to perform better with rising prices. We can see the defensive stocks were not as heavily effected, with staples 1% decline, and Financials did well considering rate changes with only 1% decline. In March’s performance, we saw the bounce back of all the sectors, but the market still remains below end of Q4 prices (NASDAQ).

Eurozone

Eurozone shares fell sharply in the quarter. The region has close economic ties with Ukraine and Russia, particularly when it comes to reliance on Russian oil and gas.

The invasion led to a spike in energy prices and caused some fears about security of supply. Germany suspended the approval of the Nord Stream 2 gas pipeline from Russia. The European Commission announced a plan – RePowerEU – designed to diversify sources of gas and speed up the roll-out of renewable energy. However, in the meantime there are fears that the high-energy prices will weigh on both business and consumer demand, hitting economic activity.

Over the quarter, energy was the only sector to register a positive return. The steepest declines came from the consumer discretionary and information technology sectors. Worries over consumer spending led to declines for stocks such as retailers, while the war in Ukraine also exacerbated supply chain disruption, hitting the availability of parts for a wide range of products.

In response to rising inflation, the European Central Bank (ECB) outlined plans to end bond purchases by the end of September. ECB President Christine Lagarde indicated that a first interest rate rise could potentially come this year, saying rates would rise “some time” after asset purchases had concluded. Data showed annual eurozone inflation at 7.5% in March, up from 5.9% in February.

The ongoing war in Ukraine and rising inflation led to a small pullback in forward-looking measures of economic activity. The flash eurozone composite purchasing managers’ index (PMI) slipped to 54.5 in March from 55.5 in February, though a level over 50 still represents expansion.

UK FTSE 100

UK equities were resilient as investors began to price in the additional inflationary shock of Russia’s invasion of Ukraine. Large-cap equities tracked by the FTSE 100 index rose over the quarter, driven by the oil, mining, healthcare and banking sectors. Strength in the banks reflected rising interest rate expectations. The Bank of England moved to hike rates ahead of other developed market central banks.

As the quarter progressed, some of the more traditionally defensive sectors advanced up the leaderboard. Intermittent fears of a global recession, however, drove periodic sell-off in some of these “safer” stocks too. Market volatility rose given the additional uncertainty related to the Russia/Ukraine conflict.

Consumer-focused areas underperformed, as did traditionally economically sensitive ones. Those parts of the market offering high future growth potential also lagged. These factors combined drove a poor performance from UK small and mid-cap equities.

Asia (ex. Japan)

Asia ex. Japan equities experienced sharp declines in the first quarter of 2022 amid a volatile and challenging market environment as Russia launched an invasion of neighbouring Ukraine.

Share prices in China were sharply lower in the quarter, while shares in Hong Kong and Taiwan also fell. The number of Covid-19 cases in Hong Kong and China spiked to their highest level in more than two years during the quarter, despite the Chinese government pursuing one of the world’s strictest virus elimination policies. The city of Shanghai, China’s financial capital with a population of 25 million people, went into a partial lockdown at the end of the quarter in a bid to curb a surge in Omicron Covid-19 cases, prompting fears that other parts of the country could also go into lockdown.

Share prices in South Korea were also sharply lower in the first three months of 2022 as the Covid-19 pandemic continues to affect economic activity in many parts of the Asia-Pacific region. However, despite the index falling sharply, there were pockets of growth such as Indonesia, which achieved solid gains in share prices during the quarter. Thailand, Malaysia and the Philippines also moved higher, although gains were more muted.

Emerging Markets

Emerging market (EM) equities were firmly down in Q1 as geopolitical tensions took centre stage following Russia’s launch of a full-scale invasion of Ukraine. The US and its Western allies responded with a raft of sanctions. Commodity prices moved higher in response to the war, raising concerns over the impact on inflation, policy tightening and the outlook for growth.

Egypt, a major wheat importer, was the weakest market in the MSCI EM index, due in part to a 14% currency devaluation relative to the US dollar. China lagged by a wide margin as daily new cases of Covid-19 spiked, and lockdowns were imposed in several cities, including Shanghai. Regulatory concerns relating to US-listed Chinese stocks also contributed to market volatility. Poland, Hungary and South Korea also underperformed.

Conversely, the Latin American markets all generated strong gains, led higher by Brazil. Other EM net commodity exporters posted sizeable gains, including Kuwait, Qatar, the UAE, Saudi Arabia and South Africa. Russia was removed from the MSCI Emerging Markets Index on 9 March, at an effectively zero price.

Global Bonds

Bond markets were volatile over the quarter. Following news of Ukraine, there was a short-lived rise in bond prices as investors looked to safe-haven assets, but overall, there is more concern over inflationary pressure that is high and rising.

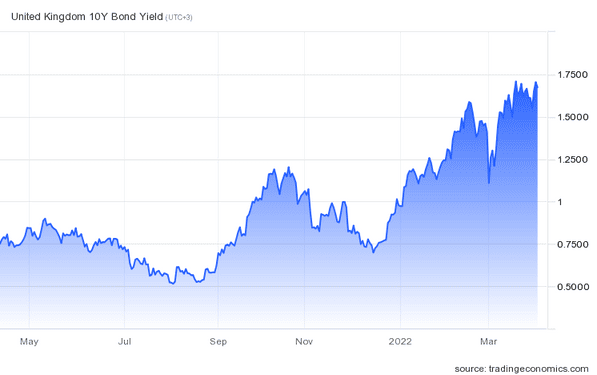

Government bond yields rose sharply (bond prices and yields move in opposite directions) so as prices dropped yields went up. Central Banks sentiment has been hawkish, bond markets responded correspondingly, pricing in present and future hikes. The extent of yield moves differed across markets. The US Treasury market is in the midst of one of its worst sell-off on record, but moves were less pronounced in core Europe and the UK.

The Fed’s rhetoric turned more hawkish and “lift-off” came as expected in March, with the Fed implementing a 25 basis point rate hike. Investors expect several more, at a swift pace, in 2022. The US 10-year Treasury yield increased from 1.51% to 2.35%, with the 2-year yield rising from 0.73% to 2.33%.

The UK 10-year yield rose from 0.97% to 1.61%, the 2-year from 0.68% to 1.36%. The Bank of England (BoE) raised rates a second time in February, in spite of concerns about the UK outlook and particularly cost of living pressures on households.

The European Central Bank (ECB) unexpectedly pivoted to a more hawkish stance in February. Comments from President Lagarde indicated rate rises were no longer ruled out for 2022 and the ECB confirmed a faster reduction in asset purchases.

The German 10-year yield increased from -0.18% to 0.55% and the 2-year yield from -0.64% to -0.07%. Concerns over potential tightening and monetary normalisation impacted Italian yields particularly, with the 10-year rising from 1.18% to 2.04%.

Corporate bonds saw significantly negative returns and wider spreads, underperforming government bonds. High-yield spreads widened more than investment grade, although they saw less negative total returns due to income. Investment grade bonds are the highest quality bonds as determined by a credit rating agency; high-yield bonds are more speculative, with a credit rating below investment grade.

Emerging market (EM) bond returns were negative. Local currency bonds were slightly more resilient than hard currency. Among EM currencies, Latin America performed well, the Brazilian real notably, but Asia and central and Eastern Europe fell.

Convertible bonds, as measured by the Refinitiv Global Focus Index, suffered disproportionally and shed 6.4% in US dollar terms compared to -5.2% for the MSCI World. Selective IT names within the universe of convertible bond issuers saw a strong rebound. The new issuance market remained subdued as market volatility was high and companies were unwilling to issue convertible bonds at low stock prices.

2022 Q1 – Cameron James

US Website Launch

We are happy to announce the launching of our USA website! The website is tailored for our US clients that details our UK Pension Transfer Advice as well as US products we service such as IRAs, 529 plans, Brokerage accounts and more. The website also features a blog page where we will be posting on a frequent basis discussing a wide range of topics from setting up IRAs, rolling over 401ks, transferring a SIPP as a US resident to many more.

We will be sending a separate email regarding the formal launch in the coming weeks and months. For those after a sneak peek, click the button below.

Visit Cameron James USA Website

UK Pension Landscape

Pension Schemes Act 2021 (An Update from 2021 Q4)

As we mentioned in our previous quarterly update, the new pension transfer system brought into power on the 1st December 2021, has given greater power to trustees to prevent pension transfers if they believe any red or amber flags arise during the transfer out process. The aim of the legislation is to reduce ‘pension scams'.

Should a red flag be raised the trustee should block a transfer, should an amber flag be raised, the individual is required to take guidance from Money Helper, the free service from Money and Pensions Service before a transfer can be approved.

There are two conditions to a transfer. The first condition is if the scheme is an authorised master trust, local government pension scheme or collective defined contribution scheme. All these are deemed low risk and therefore, unless any major red flags are spotted, it will be approved without extra due diligence. The second condition considers if there is a risk of scam which ask various questions of the member e.g. whether they were cold called, offered financial incentives to transfer, who their adviser is and their relevant FCA registration, are the investments regulated etc., it also includes as an overseas scheme if the member can provide employment link or residency link.

Who Wrote the Bill?

The reality, in my professional opinion, is that the bill was drafted and written by the lawyers of those select and old school pension schemes who would benefit from it and do not want things to change. You can think of the new legislation as saying Uber's are terrible and everyone should only use Black cabs!

Even the wording of the hundred plus page article, is far beyond the level of pension knowledge I have ever come across in the various UK Government agencies over my 10+ years experience.

Moreover, it shows a complete and utter lack of understanding of anything beyond the UK. What type of bill would possibly tell French or EU residents that they must prove a residency link for a new transfer to a Maltese QROPS? This alone shows how little they understand pension transfers.

What Has Been the Impact, and What Do We Expect in the Future?

QROPS Transfers

We highlighted in our last quarterly update that we felt QROPS could be the most challenging area moving forward due to the need to prove a residency or employment link. The QROPS schemes we work with are predominately in Malta, which is acceptable for EEA and UK members to use, most clients that utilise QROPS are not a resident of Malta hence the concern over transfer hold-ups.

Despite this, we have not experienced any difficulties in moving ahead with several QROPS cases since the beginning of the year, in conjunction with this legislation. In fact, we even had a few clients who were based in the UK who did not have a clear link in residency or employment, and who was able to move forward with his transfer without any issues.

This alone shows how even the UK pension trustees are not paying attention to all the updates, as they are illogical and don’t make sense. A client could easily sue the trustee for not allowing a QROPS transfer to save LTA, and subsequently footing a large tax bill.

Defined Benefit (DB Transfers)

Likewise, we have not experienced any major disruption in moving forward with DB transfers as a result of a change in the rules. The major reason for this is that while DB Transfers are complicated, the framework is already very stringent and well mapped out because of the FCA’s deep line of oversight on this area of advice, meaning the process on all sides from the trustees, to the report writers to the receiving schemes is already fine-tuned.

Defined Contribution (DC Transfers)

With DC transfers, we did not feel an impact at the end of 2021 in December. However, trustees seem to started putting in place tougher systems to abide by the rules from the beginning of 2022. We have seen an increase in questionnaires to cover the FCA guidelines on amber and red flags, we have seen an increase in requests for documentation including wet signed and posted documents, and have had many clients where they were required to speak with MaPS.

As trustees adjust their rules and procedure, it, unfortunately, delays transfer times for clients, when amendments or additional information is requested the admin teams on the receiving schemes can be slow in processing such information which holds up transfers.

More Staff and Departments

The company continues to grow at a rapid pace, with multiple hires across all departments in Q1. We trust you can see this on a daily basis with the level of service and fast turnaround times that we achieve on all requests. My goal is reinvesting as much money as possible in the company and further stretching the distance between ourselves and the competition in the UK Transfer Advice space.

We are also launching an IFA Summer Internship 2022 programme to attract the very best graduates talent from the UK and US University system.

Interestingly, the number of applicants reaching out directly to Cameron James and cutting out the job websites has significantly increased. With many graduates now seeking to work in a smaller niche companies, compared to working in the big investment banks in London or NYC, who are struggling to attract and retain high calibre staff.

Recent YouTube Videos

Our YouTube channel continues to grow with success, with many of our new enquiries having originally found us through the channel. The channel helps create strong relationships with clients, as they can educate themselves on complex and niche topics.

Such as the growing problem of Final Salary Pension Deficits in the UK with an ageing population and stressed pension scheme assets.

Completing their homework and due diligence, before reaching out to Cameron James for their Free Initial Appointment with myself or one of our advisors. We will be continuing to invest our time and energy in the channel, and it is one of the best places to have updates from the company.

Such as the ‘myth' that DB Pensions Values Are Rocketing, when in-fact people need to take action now to attain the best CETVs.

If you have not done so already, be sure to subscribe to the channel for our latest news and updates.

Subscribe to Our YouTube Channel

Closing Remarks

It's seems with each passing quarter that my analysis becomes longer. One thing that is for certain, is that the chapters in the history books will be packed from this recent period. We have seen an unprecedented situation is occurring globally from both an economic and political perspective.

My goal, at Cameron James, is to continue re-investing heavily in the company, ensuring we maintain our high level of initial and ongoing service, and putting further room between ourselves and the competition in the UK Pension Transfer market.

Should you ever wish to speak with me directly, please do just drop me an email or a WhatsApp message (+447870817830) and I will be happy to chat.

Take care and let's hope for a slight less dramatic remainder of the year!

Dominic James Murray

CEO & Founder

Cameron James