What Is a SERPS Pension?

SERPS stands for State Earnings-Related Pension Scheme, which was a scheme introduced by the government to replace the graduated scheme. The purpose of the scheme was to provide additional earnings to people’s basic state pension. For this reason, it’s also known as the Additional State Pension. It operated between 1978 and 2002. Those who paid Class 1 National Insurance Contributions (NIC) during this period accrued SERPS benefits.

How Is the SERPS Paid Out?

The amount that you will receive from your SERPS is dependant on a few factors:

- How many years you paid National Insurance for;

- Your earnings;

- Whether you’ve contracted out of the scheme;

- Whether you topped up your basic state pension (this was only possible between 12 October 2015 and 5 April 2017).

If you earned over the Lower Earnings Limit (LEL) you were eligible for the SERPS. The benefit was calculated based on an individual's earnings between the LEL and the Upper Earnings Limit (UEL). If you had retired before 6 April 1999, your maximum entitlement was 25% of the revalued UEL.

The benefit level was considered to be too high. In 1988 it was announced the maximum benefit would be reduced to 20%. Rather than being calculated based on the best 20 years, an individual’s revalued working life earnings would be used to determine the benefits.

Can I Get Money Back From SERPS?

You can no longer pay into the SERPS pension scheme as it stopped running in 2002, when it was replaced by the S2P (State Second Pension), which operated in a similar way. In 2016, it was replaced by the new state pension and there is no longer an Additional State Pension in place, which largely simplified the system.

What Pension Will I Get if I Opted Out of SERPS?

You may have decided or automatically been taken out of your SERPS pension scheme, in what is called contracting out. You could only contract out of your SERPS, if your employer ran a contracted-out pension scheme. This meant you paid lower National Insurance Contributions, or they were diverted into the alternative scheme.

If you're contracted out of your SERPS, then your state pension will typically be lower depending on when you retired. You would usually have contracted out for a value of benefits equal to or higher than what was inside the Additional State Pension, in most cases into a Defined Contribution scheme. Therefore, having greater choices in how you received the pot and without being limited to taking the pension as an annuity.

You can check if you were contracted out by checking an old payslip, calling your pension provider, or lastly you can use the HMRC’s Pension Tracing Service, if you have lost the pension provider's details. After 6 April 2016, when new pension legislation was introduced, it was no longer possible to contract out of your SERPS pension scheme.

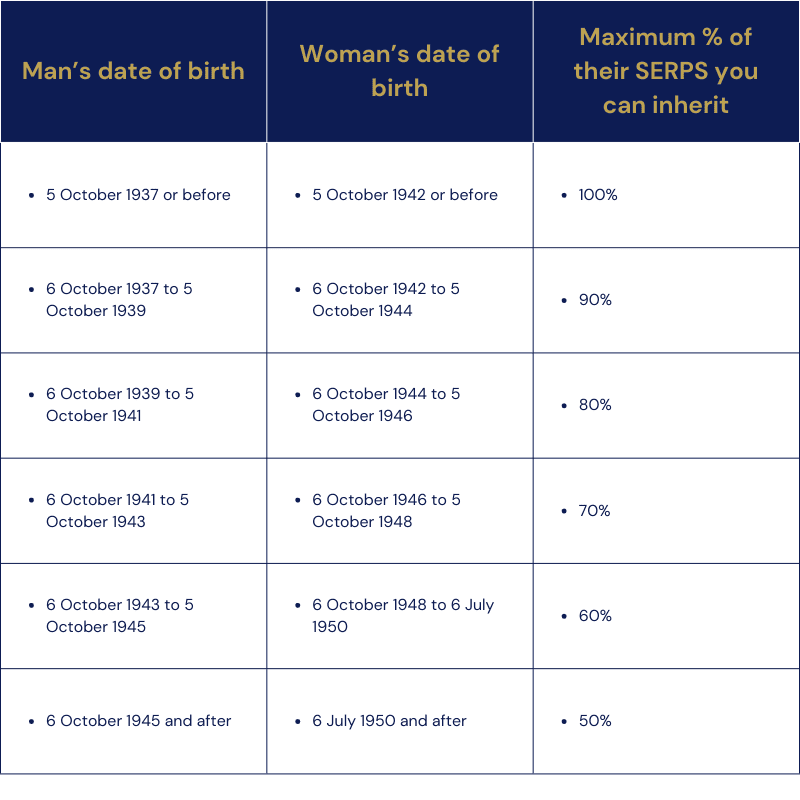

Maximum SERPS Pension You Can Inherit

The maximum you can inherit depends on when your spouse or civil partner died. If they died before 6 October 2002, you can inherit up to 100 percent of their SERPS pension scheme. If they died on or after 6 October 2002, the maximum SERPS pension scheme and state pension you can inherit depends on their date of birth. Refer to the table below for the details.

How Do I Find Out What Happened to My SERPS?

Some people are unaware they had a SERPS pension scheme and may no longer have any paperwork or connection to the firm that ran their scheme. If this sounds familiar, you can try to track down old pensions using the government’s tracker tool.

Can I Cash in My SERPS?

You cannot cash in your SERPS pension scheme. It is treated in the same way as the State Pension and can only be deferred to when you take the annuity that it gives, and will be paid out at the same time.

Get in Touch With Us for Your SERPS Pension Scheme

If you have a SERPS pension scheme or are not sure if you do and would like to discuss it with an adviser, please do get in touch. We at Cameron James speak with many clients who have a SERPS pension scheme, have contracted out of the scheme, or who didn’t even know they had one. We will be able to help you understand your pension assets and how to maximise them. Click the button below to start a free initial consultation with one of our IFAs.