Negotiating prices is common when purchasing most products or services, and the UK pension transfer industry is no exception. But is it really a good idea to try to negotiate advice fees when transferring your Defined Benefit (DB) pension? Transferring your pension is a significant decision that requires careful consideration and professional guidance. The DB pension transfer process typically takes longer and involves stringent regulations. This includes a mandatory consultation with a qualified Pension Transfer Specialist if your pension value exceeds £30,000. Understanding these factors will help you decide if negotiating fees makes sense in your situation.

The Fees Structure

There are many FCA-regulated IFAs in the UK Pension industry to choose from. Each IFA will have a fee structure you can choose from that you feel comfortable with.

In general, there are no rules that regulate the fees of an advisory service set by the IFAs. This means that the cost structure is an entirely commercial decision by the IFAs themselves. The average annual fee for a DB Pension Transfer cost is 1.9%, split into IFA fees, platform fees, and funds.

With this in mind, you must understand the fee structure of your preferred IFA. Understanding the fee structure can reflect what your IFA will do for you and how they will be involved with your UK Pension Transfer process. By understanding their fee structure, you can decide whether it is worth working together with the IFA.

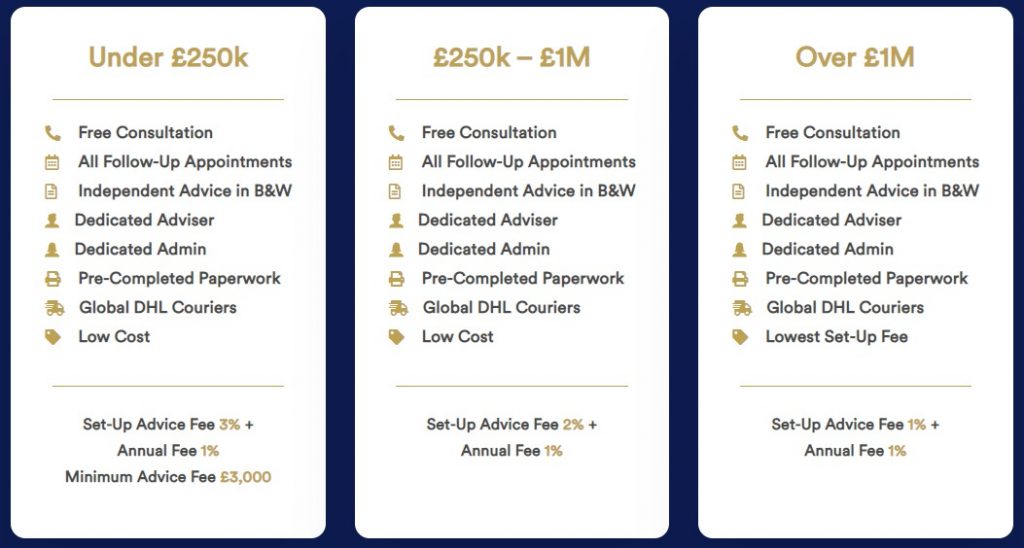

At Cameron James, the cost of services is not negotiable. However, we offer highly competitive rates for UK Pension Transfers. The below table provides a clear breakdown of our advice fees for pension transfers:

As you can see above, we offer 1% annual ongoing fees for all clients. As you move into different AUM bands, we offer a smaller percentage fee for the initial set up and transfer fee. All in with Cameron James your cost (IFA, SIPP, platform, and funds) would total approximately 1.5% p.a., beating the UK average of 0.9% for DB ongoing fees according to XPS pensions.

At Cameron James, we are one of the market's lowest-cost providers that allows our clients to proceed whether the advice is to transfer or remain.Our annual PI insurance for insistent clients is enormous, but in context, great value as we operate in 4 licensed areas which gives us economy of scale.

With our below industry-standard fees and all the benefits we offer, it does not mean we give service that is below par. In fact, as you can see on our Google Reviews, we have over 230 5-star reviews. Our affordable cost comes together with our high level of service.

CETVs for DB Pension Transfer

If you have a DB Pension and are considering transferring, we advise you to approach it cautiously. As we stated above, there are regulations set in place and requirements you must meet before you can proceed with your DB Pension Transfer. The FCA and DWP put in place these regulations to prevent you from getting scammed.

One of the other most essential things about a DB Pension Transfer is your CETV. Your CETV plays a significant role in your DB Pension Transfer process. Your pension administrator will calculate the value of your DB Pension into a lump sum that is available to transfer or invest into a new personal pension scheme, such as an International SIPP or QROPS. A number of factors influence the value of your CETV:

- Age

- Normal retirement age

- Living costs

- Life expectancy

- Investment scheme

- UK gilt rate

- Marital status

Keep in mind that the Bank of England has hiked interest rates by 0.25% to 1% on June 5th, 2022, to mitigate inflation that recently hit a high of 10%. With the higher current interest rates, your CETV value will have some downward impact, although this is balanced out by higher inflation which increases CETV values. Watch one of our videos below to understand the importance of CETV and why the current situation is the best time to get your CETV.

🎥 Check out our YouTube channel for more expert guidance on UK Pension Transfers

At Cameron James, to have your advice report it typically costs between £3000-£3500 plus VAT, depending on how many DB schemes you have, and the CETV value of each.

Why You Should Not Negotiate the Advice Fee for Your DB Pension Transfer

Choosing the right financial adviser for your DB pension transfer means weighing the value of expert advice against the cost. While negotiating fees might seem tempting, it often compromises the quality and integrity of the service. The complexities and regulatory safeguards around DB pension transfers demand thorough, professional support, something that simply cannot be rushed or undervalued.

At Cameron James, we offer some of the lowest fees in the market without cutting corners on service quality. If you want clear, transparent advice from experienced specialists, don’t hesitate to get in touch.

Book your free consultation now to discuss your pension transfer options and fees with one of our qualified IFAs.