If you're holding a SIPP and you're a non-UK resident, you might be thinking: are there any changes for me by becoming a non-UK resident? Well, there are many factors to this. Whether or not you can remain part of a UK SIPP will come down to the terms and conditions of your plan in the UK. But many people overlook one crucial area: how their choices impact death benefits.

Watch a dedicated video where we explore the crucial considerations of holding a UK SIPP as a non-UK resident. We cover the risks of using UK-based providers that don't support overseas beneficiaries, explain how international SIPPs offer smoother estate transitions, and share real-life stories that highlight why proper planning is essential. Don’t leave your loved ones unprepared, get informed and protect your legacy.

Is Your Current SIPP Still Suitable?

If you’re living abroad and still have your UK SIPP, you might feel a sense of relief thinking you’ve managed to hold on to your UK SIPP without making any changes, and everything seems to be ticking along just fine. But here’s the catch, and it’s a big one. Just because you still have your UK SIPP doesn’t mean it’s still the right fit for you.

We totally get it. There’s comfort in sticking with something familiar, especially when it’s a name you know and a provider you’ve dealt with for years. But when you move overseas, the landscape changes. Suddenly, what once worked perfectly might not serve you or your family the way you think it will, especially when it comes to passing it on. It’s not just about death benefits or whether your spouse can take over the account. It’s also about cost, access, and flexibility.

A typical UK SIPP might charge you around 10 to 20 basis points annually on the platform. That sounds reasonable, right? But here’s the interesting part: international SIPPs, those specifically designed for non-UK residents, often cost only slightly more. We’re talking maybe 10 basis points more per year.

There’s a new international SIPP we’re currently using for several clients that’s actually cheaper than many UK SIPPs. We’re not saying you have to switch providers right away. But what we are saying is this: ask yourself whether your current setup truly fits your needs now that you're living outside the UK. If the is “I’m not sure,” then it’s probably time to explore your options.

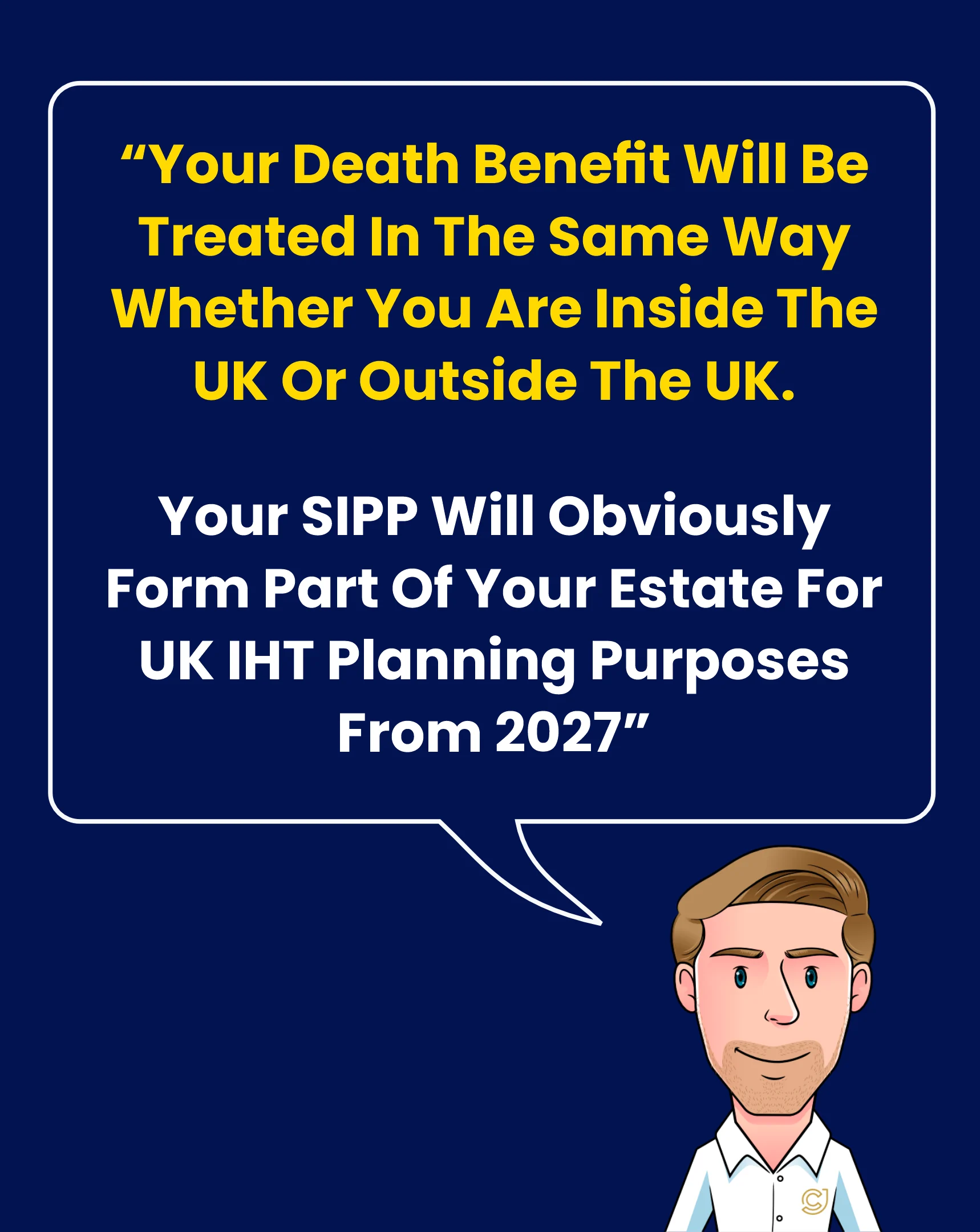

What Happens to Your SIPP When You Die?

You might wonder how living abroad affects what happens to your UK SIPP when you pass away From a death benefits perspective, it isn’t. Whether you live in the UK or overseas, your SIPP still forms part of your estate.

That means from 2027, it will fall under UK Inheritance Tax (IHT) planning rules. Your SIPP is an asset like any other, and you can pass it on to your loved ones: your spouse, children, or other beneficiaries, according to your will. A lasting power of attorney ensures someone you trust carries out your wishes.

However, what's really important to understand is: will your death benefits work the same way if you’re living overseas with your partner, spouse, or children, as they would if you were still living in the UK? The answer is categorically no.

Very few UK SIPP providers actively support non-UK residents or their overseas beneficiaries. Some allow you to stay in the scheme if you joined before moving abroad, but they refuse new applications from overseas. That restriction can cause major issues for your loved ones after you pass away.

At Cameron James, we work with numerous non-UK residents. Year after year, we get inquiries from people who are trying to navigate this exact issue. They’ve moved abroad, kept their UK pension, and assumed everything would carry on as normal. But when it comes time to pass that pension on, they suddenly hit a wall.

My Partner Passed Away—Now What Happens to Their SIPP?

This is where we see the emotional and practical sides of financial planning collide. A common scenario looks like this: someone opened a SIPP with them a decade ago while living in the UK. All good. Then they moved abroad, let’s say to the U.S., and just carried on as normal, keeping the pension in place. Fast forward to today, that person has passed away, and their spouse, who is also living abroad, reaches out to the provider to transfer or manage the pension. The response? “Sorry, we don’t accept applications from non-UK residents.”

And this is where the drama begins. Unfortunately, we’ve seen some horrible situations in the past two years, bereaved spouses or children calling us distressed because they can’t access or manage inherited SIPP funds.

If a provider’s policy is not to accept new non-UK resident applications, then they’re essentially admitting that their product isn’t suitable for people living overseas. That logic doesn’t hold up when it comes to your loved ones trying to carry on with your financial plan. And it’s often your family who end up stuck in the middle of this grey zone. They are the ones left trying to figure out what’s allowed, what’s not, and how to access money that should have been a smooth and secure part of your legacy.

Why International SIPPs Matter for Your Family?

Unlike many UK-based providers, international SIPPs are built for non-UK residents. International SIPPs fully aware that you’re living overseas. More importantly, they’re structured to support you and your family, no matter where you are in the world.

One of the biggest advantages? They allow new applications from people living abroad. That might not sound groundbreaking at first, but when it comes to your long-term planning, especially what happens to your pension when you pass away, it makes all the difference.

Here’s a typical case we often see: a client who moved to the U.S. years ago and built up a £1 million UK pension pot. He’s married with two children and has clearly instructed that, upon his passing, 50% of the pension goes to his wife and 25% to each child.

Now, if he’s using an international SIPP, things are much more straightforward. His beneficiaries, who are also living in the U.S., would be able to seamlessly transfer the pension into their names. They could keep the funds invested within the pension wrapper, continue working with their financial adviser, and manage the drawdown however it suits their needs.

They don’t have to cash everything out and can avoid awkward compliance issues. And most importantly, they don’t get stuck with a provider saying, “Sorry, we can’t help you because you’re no longer based in the UK.” It’s a far smoother, more flexible, and more tax-efficient process.

Don’t Wait Until It’s Too Late!

If you’re a non-UK resident enjoying life abroad, whether that’s in the U.S., Europe, the Middle East, or elsewhere, it’s easy to assume that your UK pension will just keep working for you. But here’s the reality: many UK-based SIPP providers no longer support non-UK residents, and that can create serious complications when it comes to passing your pension on to loved ones.

We’ve seen firsthand how this can play out. Over the years, we’ve helped clients, and their families, navigate some incredibly stressful and emotional situations. It’s heartbreaking when grieving spouses or children are suddenly blocked from accessing or managing a SIPP because the provider won’t deal with non-UK residents.

That’s why we put this article together, to help you understand the often-overlooked risks around SIPP death benefits for non-UK residents. Proactive planning now could save your family an enormous amount of time, stress, and financial loss later.

Book a Free Consultation

If anything here has raised questions about your current SIPP or made you rethink your long-term plan, we’re here to help. You can book a free consultation with one of our experienced financial advisers using the link below. We’ll take the time to understand your situation, walk you through your options, and help you make an informed decision that’s right for you and your family..

Your UK pension is one of your most valuable assets. Protect it, and ensure it supports your loved ones when it matters most.