Employers automatically enrol workers into workplace pension schemes through Pension Auto Enrolment. Governments enforce this legislation to boost private savings and improve retirement living standards.

There has been an increasing adoption of Pension Auto Enrolment in developed countries, where we are generally seeing an increase in life expectancies and ageing populations. This is no coincidence and is in place to help reduce the burden on the state as the life expectancy of pensioners continues to increase.

In the UK, approximately 19% of the population is aged 65 or over. There has been a 23% rise in this age group over the last 10 years, and over this time the UK population also grew by 7%. Behavioural studies have recognised that even when people can choose to join workplace schemes, many employees do not join. However, when employers automatically opt people in and require them to opt out, significantly more employees remain in their workplace schemes.

What Is Pension Auto Enrolment UK?

Auto Enrolment Pension was brought in under The Pension Act of 2008, which reformed workplace pensions. The law became effective from 1 April 2012. The law states that all employers must offer all eligible jobholders a qualifying workplace pension and that the employer must pay a minimum contribution on behalf of their employees.

Pension Auto Enrolment was slowly phased in to ensure that it did not cause disruption to how firms functioned. The largest employers were the first to lead the way, naturally followed by medium, small and micro employers. By February 2018, all employers had phased in Pension Auto Enrolment. HMRC determined the size of each employer based on the number of workers on the company’s PAYE records. The Pensions Regulator wrote to each employer 18 months before the enforcement date of their requirements for Auto Enrolment Pension.

Who Is Eligible for Auto Enrolment UK?

Essentially, every employee is eligible for Pension Auto Enrolment in a scheme, with the following exceptions:

- A worker who has opted out or ceased active membership of a qualifying scheme;

- A worker who has given notice or been given notice of the end of their employment;

- A worker where the employer has reasonable grounds to believe the worker is protected from tax;

- A worker with charges on their pension savings under HMRC’s primary, enhanced, fixed or individual protection;

- A worker who holds the office of a director of the employer;

- A worker who is a member (partner) of a limited liability partnership (LLP) and is not treated for income take purposes as being employed by that LLP;

- A worker who has been paid a winding up lump sum payment while in the employment of the employer and during the 12-month period that started on the date the payment was made;

- A worked who ceased employment with the employer after the payment has been paid, and was subsequently re-employed by the same employer;

- A worker who meets the definition of a ‘qualifying person’ for the purposes of separate UK legislation;

- A worker on occupational pension schemes and cross-border activities within the European Union (EU).

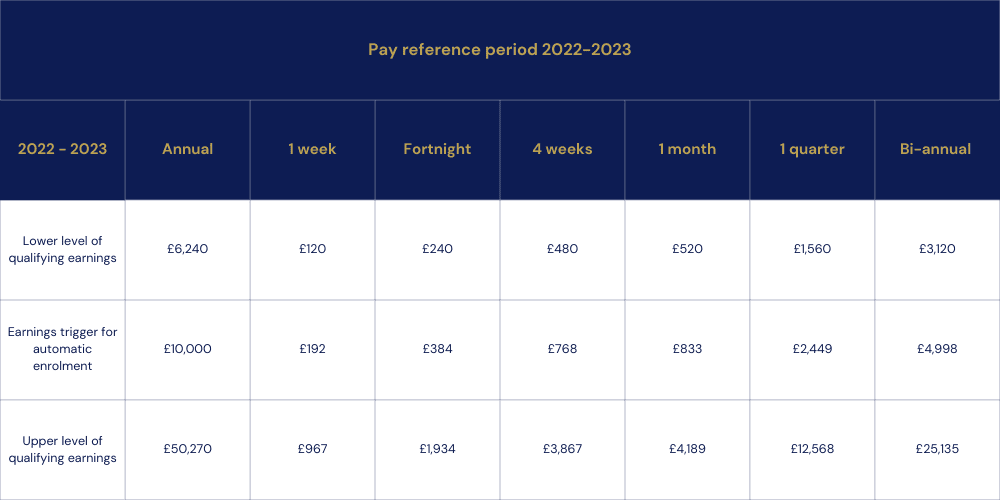

To be automatically enrolled, you must also earn above the trigger amount which is currently £10,000. You must also be between the age of 22 and the State Pension Age. If you fall within the qualifying earnings band, which is higher than the lower level but does not exceed the upper level, barring other factors, you should qualify for pension contributions. If you are between the lower level and earnings trigger, you may have to opt-in to the company pension. Refer to the table below for the detail.

When Did Pension Auto Enrolment Start?

As the name suggests, you do not actually have to do anything to be signed up for your workplace pension scheme. As part of the legislation, the eligible jobholder must not be required to provide any information to join the scheme or remain a member. It is the employer’s responsibility to pass all relevant information to the scheme trustees, managers, and/or provider.

The employer has a six-week window from the employee’s start date to auto enrol the individual. The employer will take the following steps:

- Give the pension scheme information about the eligible jobholder

- Give the eligible jobholder enrolment information.

- Make arrangements for the eligible jobholder to become an active member by the Pension Auto Enrolment date.

How Often Is a Pension Re-Enrolment?

Further to the initial enrolment, employers are also required to re-enrol eligible jobholders into their schemes on a regular basis. Currently, jobholders must be re-enrolled every three years. There is also the possibility of immediate re-enrolment for a few reasons:

- The employer caused membership to cease through an act or omission

- The scheme ceased to be a qualifying scheme through an employer act or omission

- The scheme trustees, managers, or another third party have caused membership to cease

- The jobholder ceased to be working or ordinarily working in the UK

- The jobholder ceased to have qualifying earnings in the pay reference period

- The employer and the worker agree that notice to terminate employment, retirement, dismissal, or resignation have been withdrawn.

What Are the Minimum Pension Contributions Under Auto Enrolment?

Under Pension Auto Enrolment, using standard qualifying tests, the employer is required to contribute at least 3% of the employee’s qualifying earnings annually, the employee must contribute at least 4% of their qualifying earnings, and with tax relief on employee contributions adding to 1%, the total minimum contribution level is 8% of an employee’s qualifying earnings.

The minimum contribution applies to anything over £6240 and up to a limit of £50,270 for 2022 to 2023. Some employers apply your pension percentage contribution, this would be something you would need to discuss with your employer.

Qualifying Auto Enrolment Schemes

The employer must ensure that the scheme in place continues to be suitable and meet legal requirements. This will include regular reviews to ensure it is of good quality. Employers often decide to utilise existing schemes, you can, however, start new schemes as long as they meet requirements. Trust-based occupational schemes are commonly used such as the National Employment Savings Trust (NEST), there are also master trust or contract-based money purchase schemes.

Final Salary Pension Schemes and Pension Auto Enrolment

Due to the nature of Defined Benefit schemes, it is unlikely that these will meet the requirements for Pension Auto Enrolment. In particular, there is a waiting period before an employee can join, which contradicts the purpose of the legislation. However, employers can set up a scheme for the initial waiting period.

If a Defined Benefit scheme is used, it must also provide benefits that are equal to or better than a set of specifications, which we have outlined below:

- Pension age of 66 (rising in line with state pension age)

- Annual pension of 1/120th of average qualifying earnings in the three tax years before the end of the pensionable service to a maximum of 40 years

- Revaluation in deferment/accrued benefits by a specified method

- Statutory increases to pensions in payment

Should You Opt-In or Opt-Out of Your Auto Enrolment UK?

Whether you prefer to stay or to transfer out your Pension Auto Enrolment, a thorough analysis of your risk profile, financial situation, and financial goals is paramount. At Cameron James, we helped multiple clients with the best financial advice concerning their UK pension assets. Book yourself in for a free initial consultation with one of our IFAs to ensure any decision concerning your UK pension assets is in your best interest through the button below.